Summary:

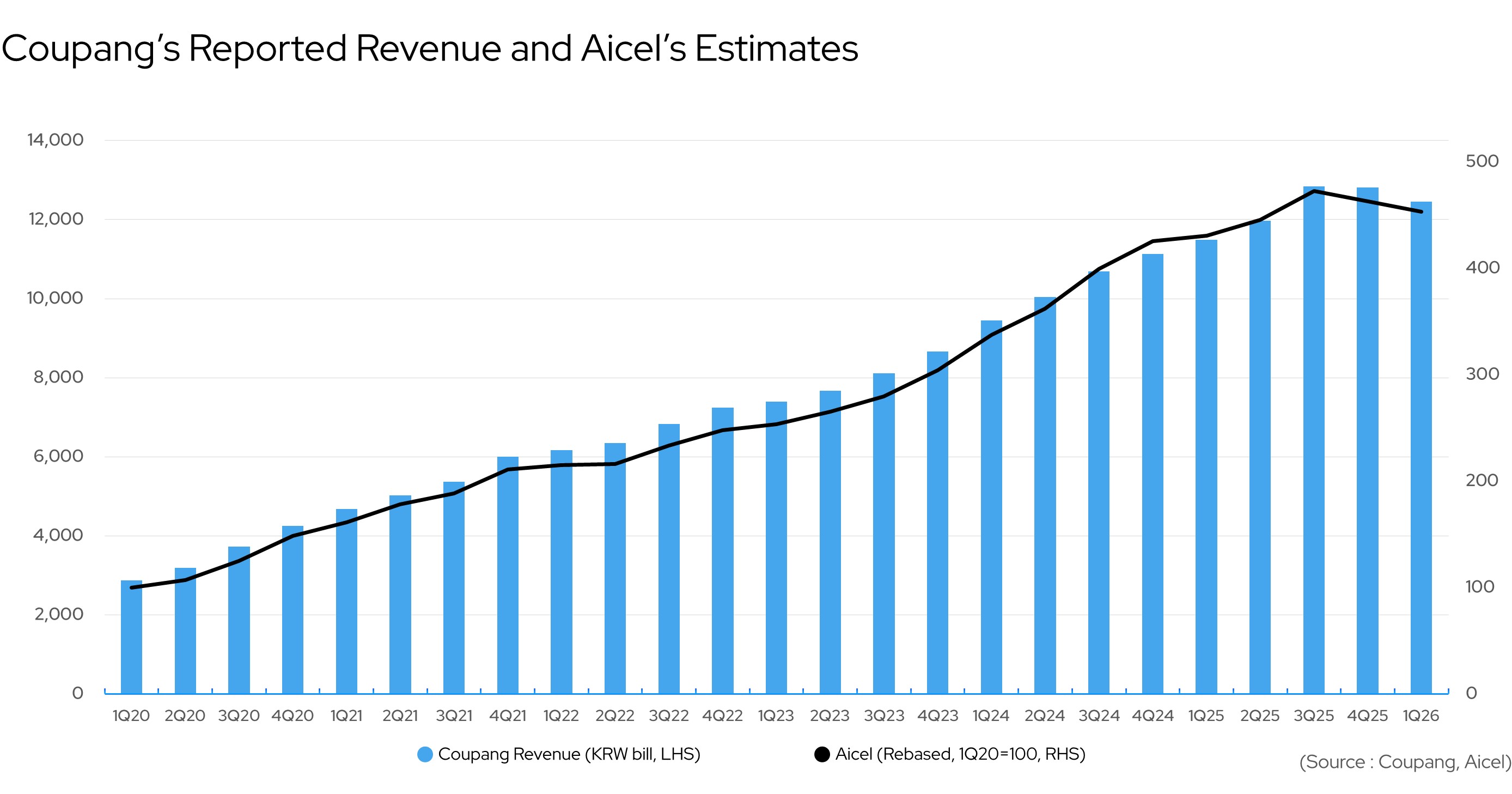

· Coupang (CPNG:US) reported Q1 2026 revenue of KRW 12.46 trillion, with revenue up 7.5% YoY and down 3.7% QoQ. In KRW terms, revenueincreased 8.5% YoY but declined 2.8% QoQ from KRW 12.82 trillion in 4Q25.

· Product Commerce active customers declined from 24.6 million in 4Q25 to 23.9 million in 1Q26, down 700 thousand, or 2.8% QoQ.

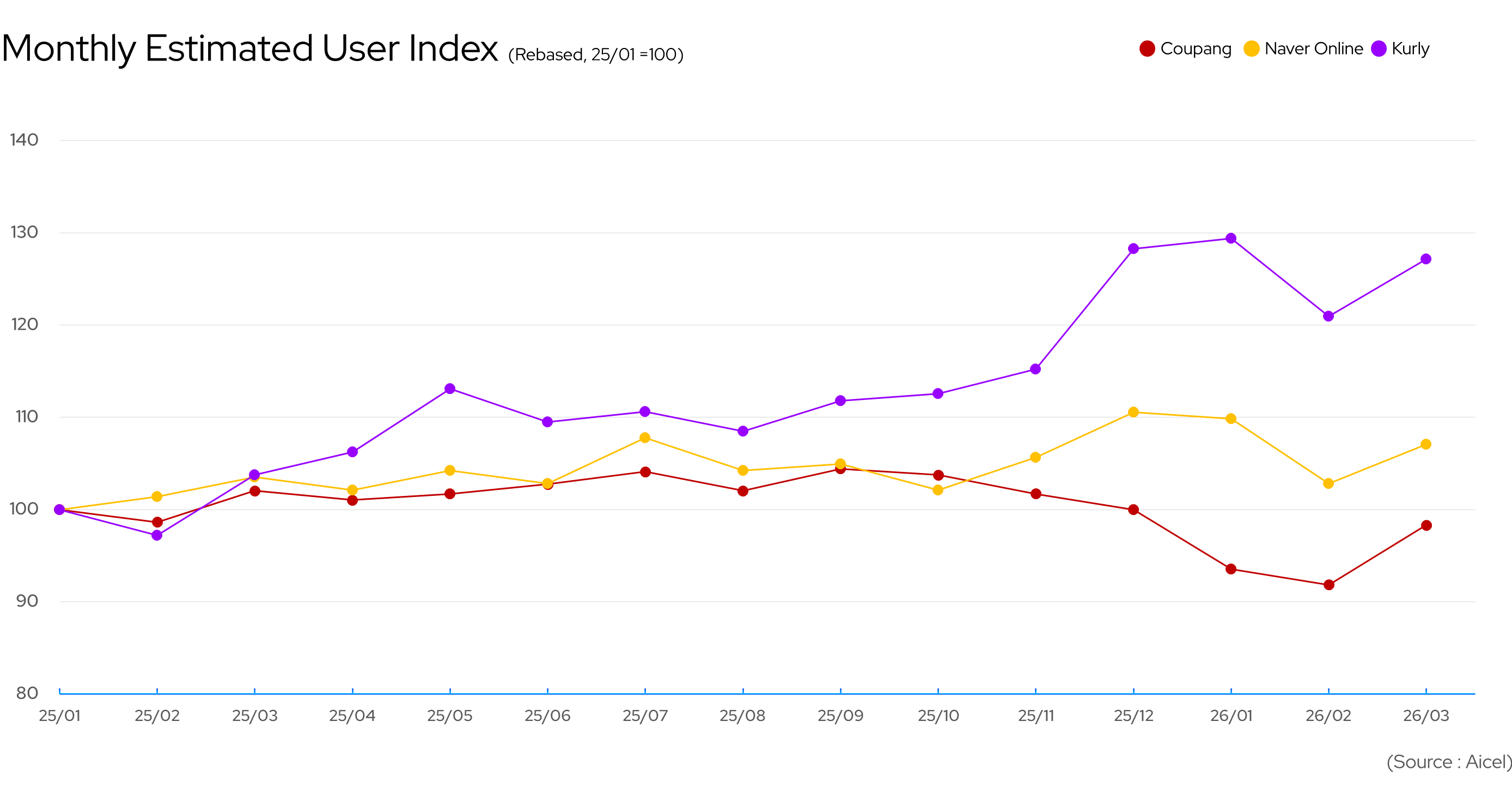

· Coupang’s monthly user index fell to 93.5 in January 2026 and 91.8 in February 2026, before recovering to 98.3 in March 2026.

· Management described January 2026 as the low point for Product Commerce revenue growth, with improvement through February and March.

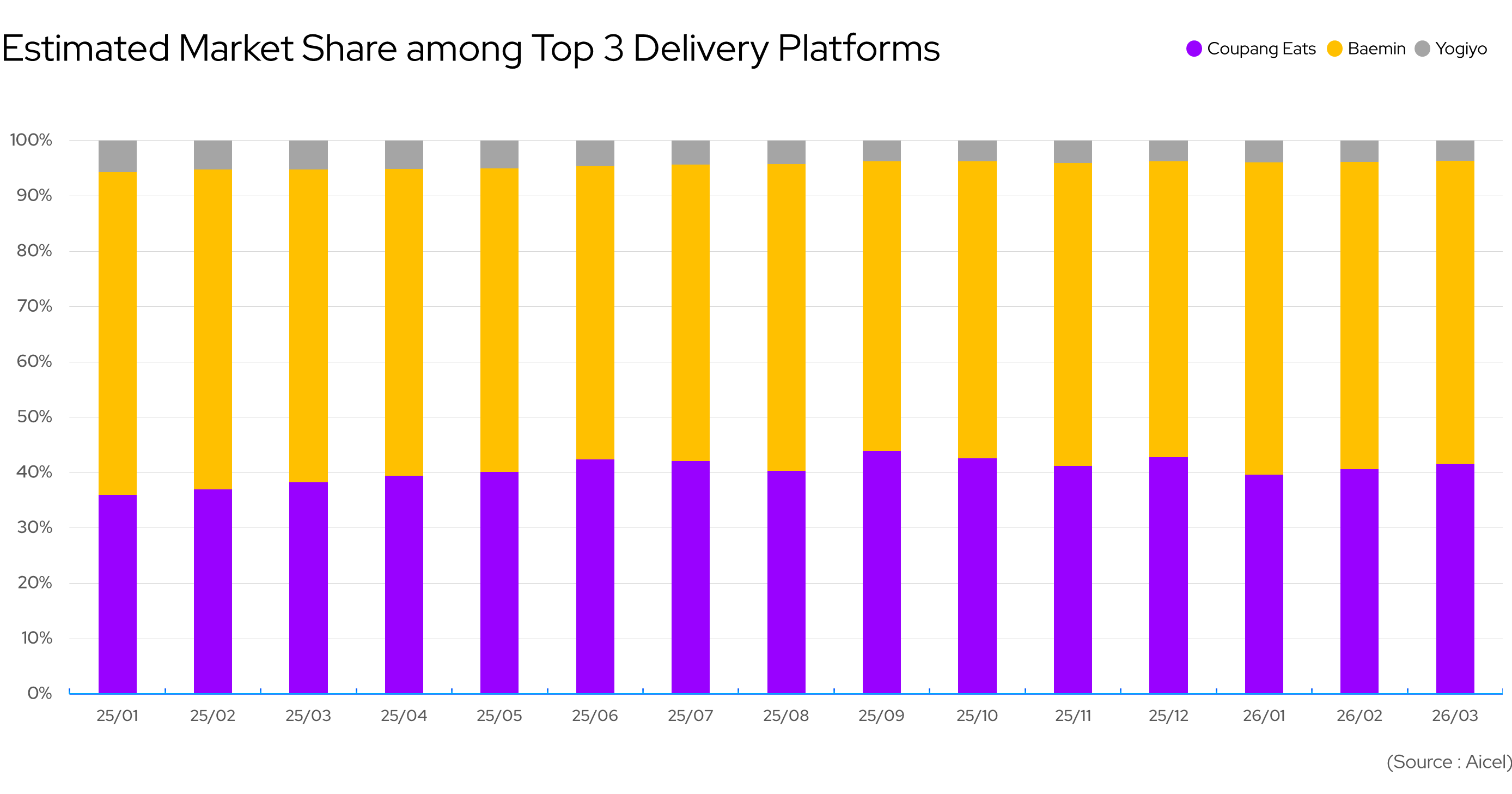

· Coupang Eats remained resilient, with market share among the top 3 delivery platforms recovering from 39.7% in January 2026 to 41.6% in March 2026.

· Overall, the weakness appears concentrated in core commerce traffic and trust, rather than across the entire Coupang ecosystem.

Revenue Trend: Stabilization Is Visible, but Reacceleration Is Not Yet Proven

Coupang (CPNG:US) delivered a mixed Q1 2026 result. Revenue increased 7.5% YoY, showing that the business continued to grow despite the data-incident shock. In KRW terms, reported revenue reached KRW 12.46 trillion, up 8.5% YoY.

However, sequential performance weakened. Revenue declined 3.7% QoQ, and in KRW terms, revenue fell from KRW 12.82 trillion in 4Q25 to KRW 12.46 trillion in 1Q26, a 2.8% QoQ decline.

Management’s earnings-call commentary framed January 2026 as the low point for Product Commerce revenue growth,followed by sequential improvement in February and March. The monthly data supports a stabilization narrative, but the quarterly revenue decline means it is still too early to call this a full reacceleration.

The key interpretation is that Coupang has moved past the worst deterioration phase, but has not yet returned to its prior growth trajectory.

Product Commerce: Active Customer Decline Remains the Clearest Weakness

The clearest weakness in Q1 2026 was Product Commerce customer engagement. Active customers declined from 24.6 million in 4Q25 to 23.9 million in 1Q26, down 700 thousand, or 2.8% QoQ.

Because active customers are measured on a trailing 3-month basis, the late-4Q25 data incident would naturally weigh on the 1Q26 figure. Even so,the decline confirms that the incident had a measurable impact on customer behavior.

The monthly user index shows the same pattern. Coupang fell from 100.0 in December 2025 to 93.5 in January 2026 and 91.8 in February 2026, before rebounding to 98.3 in March 2026.March improved meaningfully from the trough, but remained below the December baseline.

Peer data also suggests the pressure was company-specific. By March 2026, Naver reached 107.0 and Kurly reached 127.1, both outperforming Coupang’s 98.3 index. This implies that Coupang’s weakness was not simply a broad Korean e-commerce slowdown.

Management Commentary: Temporary Dislocation Is Plausible, but Not Fully Proven

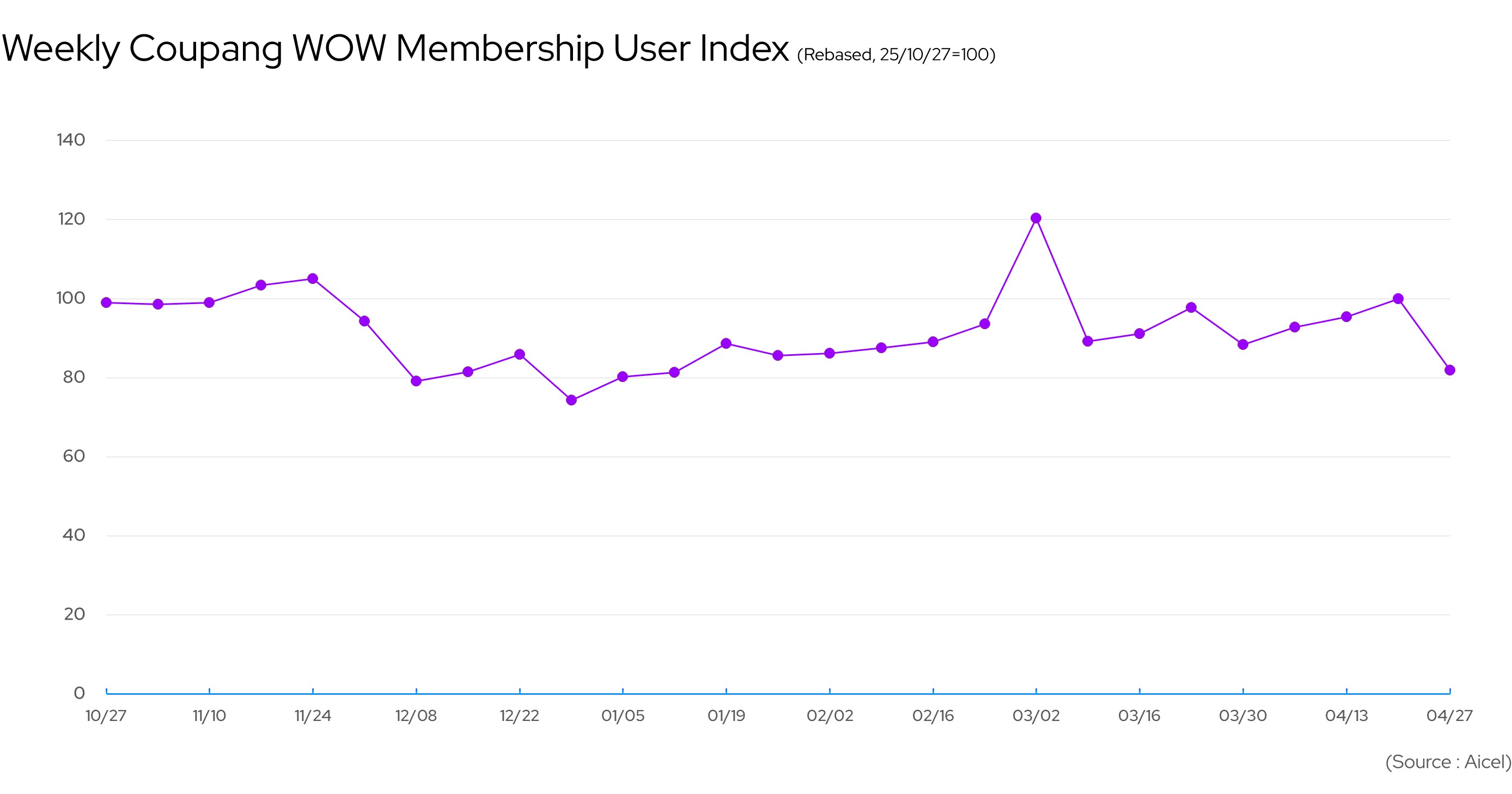

Management's temporary-dislocation argument is plausible. The weakest point came after the late-2025 data incident, with the WOW Membership User Index falling sharply in early December before gradually recovering through early 2026. The index also showed a temporary spike in early March, suggesting that part of the membership shock had reversed.

However, the evidence remains incomplete. The weekly WOW Membership User Index did not show a clean and sustained return above the late-October baseline, and the latest April reading weakened again. This makes the recovery narrative directionally reasonable, but not yet fully validated.

The same pattern is visible in broader operating data. The March monthly user index improved from the February trough, but remained below the December 2025 baseline. Product Commerce active customers were still down 2.8% QoQ, and revenue declined 3.7% QoQ.

Therefore, Coupang should be viewed as being in early-stage recovery, not yet in confirmed reacceleration. For Q2 2026, the key question is whether improving traffic and WOW membership stabilization can translate into stronger revenue momentum and margin normalization.

Profitability Pressure: Vouchers and Supply-Chain Inefficiencies Created Real Margin Drag

Profitability was pressured by vouchers and supply-chain inefficiencies. These costs suggest that Coupang had to use incentives andoperational adjustments to support customer reactivation and servicereliability after the data incident.

This creates a two-sided investment interpretation. If customer trust and engagement continue to recover, voucher-related pressure could prove temporary and operating leverage may improve. However, if traffic remains below pre-incident levels, Coupang may need to sustain higher incentives for longer,delaying margin recovery.

For investors, the issue is not only whether revenue recovers, but whether it recovers without excessive promotional spending.

Coupang Eats: Resilient Share Suggests the Weakness Is Not Systemic

Coupang Eats was the strongest part of the dataset. Among the top 3 delivery platforms, Coupang Eats’ market share declined from 42.8% in December 2025 to 39.7% in January 2026, but recovered to 40.7% in February and 41.6% in March.

This matters because it argues against a broad deterioration across the entire Coupang ecosystem. If customer trust had weakened structurally across all Coupang services, Eats would likely have shown a more severe and sustained decline.

Instead, the data points to a more concentrated problem in core Product Commerce traffic and trust. A resilient Eats business also remains strategically important because food delivery can support app frequency, customer engagement, and ecosystem lock-in.

Peer Comparison: Coupang’s Rebound Still Lagged Naver Online and Kurly

The March recovery was positive, but relative performance remained weak. Coupang’s monthly user index recovered to 98.3 in March 2026, while Naver Online reached 107.0 and Kurly reached 127.1.

This gap indicates that Coupang’s recovery was incomplete both inabsolute terms and relative to peers. Kurly’s strength is particularly notable because it suggests that Korean online commerce demand did not broadly deteriorate in the same way.

This does not necessarily mean long-term market share loss. Coupang still retains advantages in fulfillment infrastructure, delivery speed, product assortment, and membership economics. However, the peer comparison shows that Coupang needs to actively regain traffic momentum.

Q2 2026 Watchpoints: Traffic, Revenue, and Margin Normalization

For Q2 2026, investors should monitor three indicators.

First, Product Commerce traffic and WOW membership trends need to move above the Q1 2026 average. A sustained user index above the December 2025 baseline of 100.0, together with stabilization in the weekly WOW Membership User Index, would be stronger evidence of normalization.

Second, revenue needs to stop declining sequentially. Coupang’s 3.7% QoQ revenue decline in Q1 2026 was a key concern despite 7.5% YoY growth. In KRW terms, revenuedeclined from KRW 12.82 trillion in 4Q25 to KRW 12.46 trillion in 1Q26,despite 8.5% YoY growth.

Third, profitability needs to recover as vouchers and supply-chaininefficiencies fade. If revenue improves but margins remain pressured, the market may conclude that recovery is being driven by incentives rather than organic demand normalization.

Investment View: Recovery Underway, but Confirmation Is Still Needed

The Q1 2026 data supports a balanced view of Coupang. The company is not showing signs of systemic platform deterioration, especially given the resilience of Coupang Eats.However, Product Commerce clearly experienced a measurable disruption, with active customers down 700 thousand QoQ, the monthly user index below the December baseline, and revenue down 3.7% QoQ.

For long-term investors, the key question is whether the data incident created a temporary engagement shock or exposed a more durable customer-trust risk. Current data leans toward temporary disruption, but confirmation is still required.

The strongest positive evidence is the March user rebound and Eats share recovery. The strongest negative evidence is the sequential revenue decline and active customer contraction.

Conclusion: Q1 Recovery Is Visible, but Not Yet Complete

Coupang’s Q1 2026 results show a business moving past the worst phase of the data-incident shock, but recovery remains incomplete. Revenue increased 7.5% YoY, yet declined 3.7% QoQ. In KRW terms, revenue increased 8.5% YoY to KRW 12.46 trillion, but declined 2.8% QoQ.

Product Commerce active customers fell from 24.6 million to 23.9 million, while the monthly user index rebounded in March 2026 but remained below the December 2025 baseline. At the same time, Coupang Eats maintained market share near 40%, suggesting that the weakness is concentrated in core commerce rather than spread across the entire platform.

The most balanced interpretation is that management’s temporary-dislocation narrative is plausible, but not fully validated. Q2 2026 data will be critical in determining whether Coupang can convert early traffic recovery into sustained revenue reacceleration and margin normalization. All data in this analysis is sourced from KED Aicel, providing diverse investment insights and enabling continuous strategic evaluation.